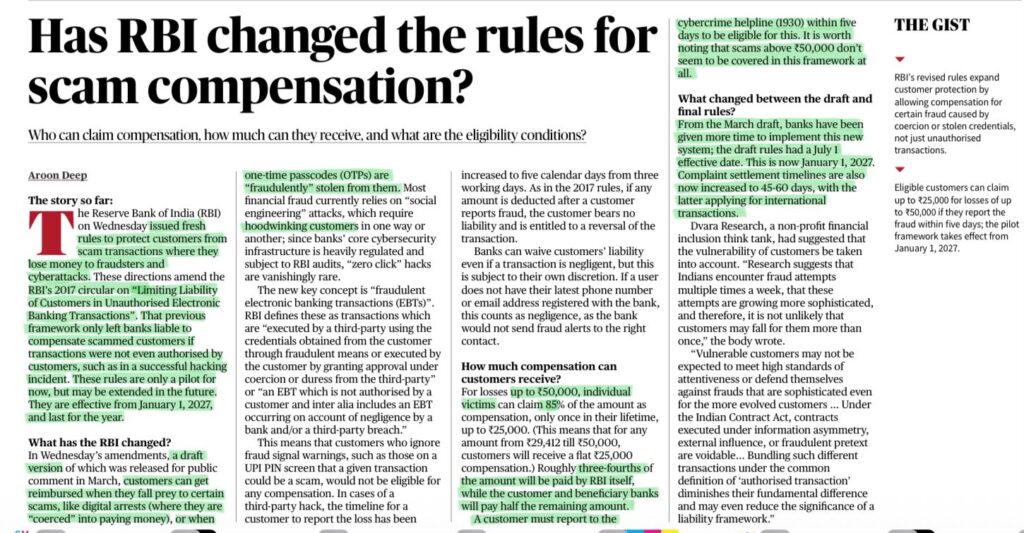

Context: RBI scam compensation rules 2027

The Reserve Bank of India has revised its 2017 customer liability framework to extend protection to victims of certain online banking scams involving fraud or coercion.

The pilot framework will be effective from 1 January 2027.

Existing Rule, 2017

The 2017 framework covered only Unauthorised Electronic Banking Transactions.

Meaning

Unauthorised transactions are those where money is transferred without the customer’s authorisation.

Limitation

Authorised scams were not covered.

This means if a customer transferred money after being deceived, compensation was generally not available under the old framework.

Revised Rule, 2027 Pilot

The revised framework covers Fraudulent Electronic Banking Transactions.

Includes

- Digital arrest scams

- OTP theft

- Social engineering scams

- Fraud or coercion-based transfers

Effective Date

- 1 January 2027

Duration

- Pilot framework for one year

Compensation Rules

Eligible Loss

- Up to ₹50,000

Customer Compensation

- 85% of the loss

- Subject to a maximum of ₹25,000

Reporting Condition

Customer must report the incident to the Cybercrime Helpline 1930 within 5 days.

Not Covered

- Losses above ₹50,000

- Cases involving customer negligence

One-line Takeaway

2017: Protection only against unauthorised transactions.

2027: Protection extended to certain authorised-but-fraudulent scams, with limited compensation.

Significance

- Recognises changing nature of cyber fraud.

- Protects victims of social engineering and coercive scams.

- Encourages quick reporting through cybercrime helpline.

- Strengthens consumer protection in digital banking.

- Pushes banks to improve fraud monitoring and response systems.

Mains Usage

This can be used in answers on:

- Digital banking security

- Cyber fraud

- Consumer protection

- Financial inclusion

- RBI regulation

- Digital literacy

- Trust in digital payments