Context:Rural Credit Inclusive Growth India

On the occasion of NABARD’s 45th Foundation Day, the Government highlighted reforms in rural credit, digital outreach and financial inclusion for a stronger and sustainable rural economy.

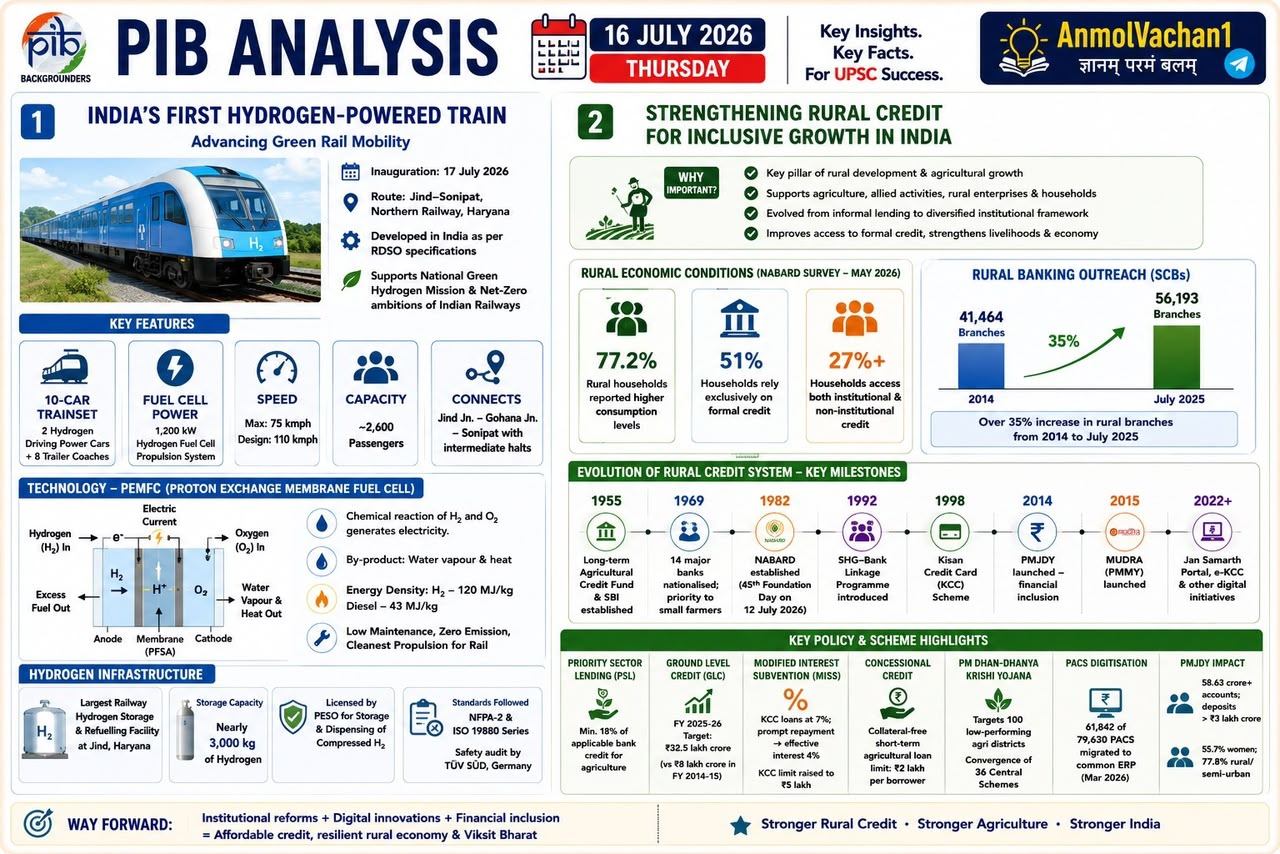

Why Rural Credit Matters

Rural credit is important because it ensures timely and affordable finance for:

- Agriculture

- Allied activities

- MSMEs

- Rural enterprises

It helps reduce dependence on informal moneylenders and supports productivity, rural income and employment.

Rural Credit – Key Data

As per NABARD Rural Economic Conditions Survey:

- 77.2% rural households reported higher consumption.

- 51% households depend exclusively on formal institutional credit.

- 27%+ households access both institutional and informal credit.

Rural Banking Network

Scheduled Commercial Bank rural branches increased from:

- 41,464 branches in 2014

- 56,193 branches by July 2025

This reflects over 35% increase in rural branches from 2014 to July 2025.

Evolution of Rural Credit

1955

Long-Term Agricultural Credit Fund and State Bank of India.

1969

Nationalisation of 14 major banks.

1982

NABARD established as the Bank for Agriculture and Rural Development.

1992

Self-Help Group–Bank Linkage Programme.

1998

Kisan Credit Card Scheme.

2014

Pradhan Mantri Jan Dhan Yojana.

2015

Pradhan Mantri Mudra Yojana.

2022 onwards

Jan Samarth Portal, e-KCC and other digital initiatives.

Key Policy and Scheme Highlights

1. Priority Sector Lending

Minimum 18% of Adjusted Net Bank Credit is targeted for agriculture.

2. Ground Level Credit

Ground level credit reached ₹32.5 lakh crore.

3. Modified Interest Subvention Scheme

Crop loans are available at 7%.

Interest can reduce to 4% on prompt repayment.

4. Collateral-Free Agricultural Loan

Limit increased to ₹2 lakh per borrower.

5. PM Dhan-Dhaanya Krishi Yojana

Targets 100 low-performing agricultural districts through convergence of 36 Central schemes.

6. PACS Digitisation

61,842 out of 79,630 PACS migrated to a common ERP system by March 2026.

7. PMJDY Impact

Pradhan Mantri Jan Dhan Yojana has enabled:

- 58.63 crore accounts

- ₹3 lakh crore deposits

- 55.7% women beneficiaries

- 77.8% accounts in rural and semi-urban areas

NABARD – Key Facts

Established

1982

Headquarters

Mumbai

Parent Act

National Bank for Agriculture and Rural Development Act, 1981

Role

NABARD is the apex development financial institution for agriculture and rural development.

Challenges

- Dependence on informal credit still persists.

- Regional disparities in credit flow.

- Limited access for tenant farmers and smallholders.

- Need for stronger digital infrastructure.

- Need for improved financial literacy.

Way Forward

- Ensure universal access to affordable institutional credit.

- Expand digital credit through e-KCC, PACS and Jan Samarth.

- Strengthen Farmer Producer Organisations and rural MSME value chains.

- Integrate credit with insurance, markets and agri-infrastructure.

- Improve financial literacy and digital access.

Key Takeaway

Stronger rural credit means stronger agriculture, stronger rural enterprise and stronger inclusive growth.