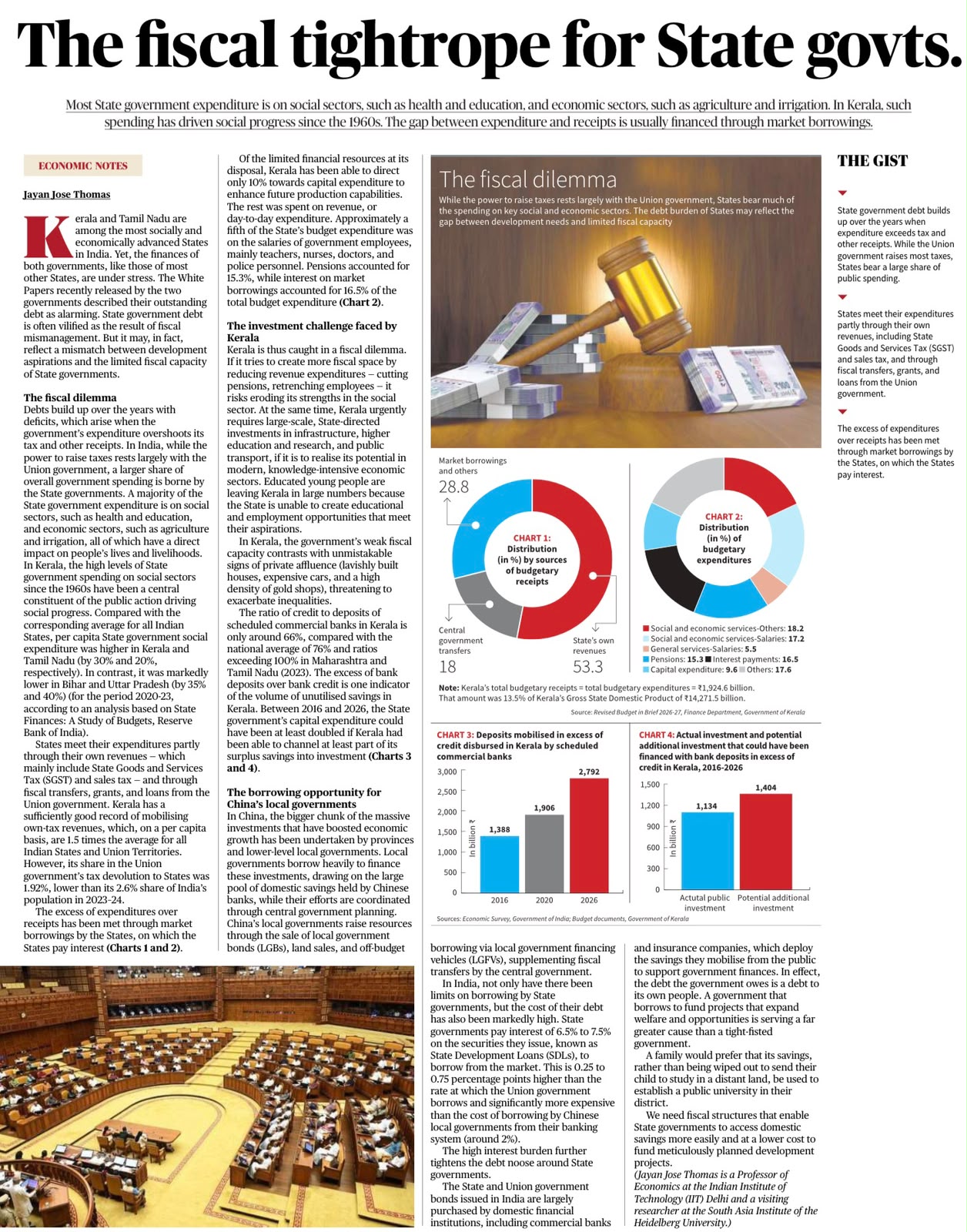

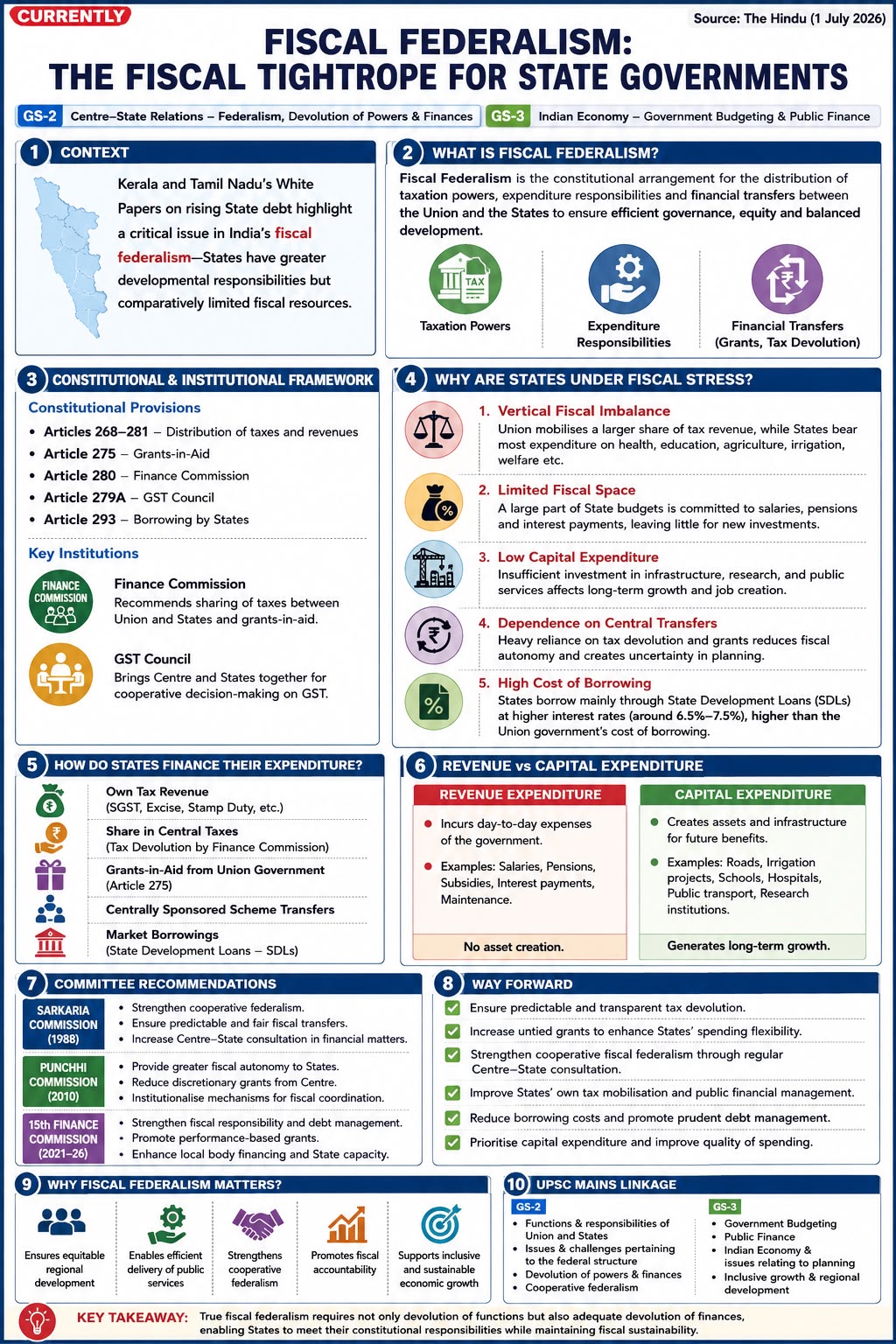

Context: Fiscal Federalism in India

The article highlights the fiscal stress faced by State governments, especially due to rising expenditure on welfare schemes, salaries, pensions, interest payments and limited revenue flexibility.

It uses Kerala and Tamil Nadu as examples to show the larger issue of fiscal federalism in India.

Fiscal Federalism

Fiscal federalism means the constitutional arrangement for distribution of:

- Taxation powers

- Expenditure responsibilities

- Financial transfers

between the Union and State governments.

Why Are States Under Fiscal Stress?

1. Vertical Fiscal Imbalance

The Union collects a larger share of tax revenue, while States bear major expenditure responsibilities in sectors such as:

- Health

- Education

- Agriculture

- Rural development

- Police

- Local infrastructure

- Welfare delivery

2. Limited Fiscal Space

A large part of State budgets is committed to:

- Salaries

- Pensions

- Interest payments

- Subsidies

- Welfare schemes

This reduces funds for capital expenditure and development projects.

3. Low Capital Expenditure

States often spend heavily on revenue expenditure, leaving less money for:

- Roads

- Irrigation

- Health infrastructure

- School infrastructure

- Digital infrastructure

- Public transport

4. Dependence on Central Transfers

States depend on:

- Tax devolution

- Grants-in-aid

- Centrally Sponsored Schemes

- GST compensation-related mechanisms

5. Borrowing Constraints

States borrow under Article 293 of the Constitution.

Borrowing limits and conditions can restrict State fiscal flexibility.

Constitutional Provisions

Article 268–281

- Distribution of taxes and revenues between Union and States.

- Grants-in-aid from the Union to States.

- Finance Commission.

Article 293

- Borrowing by States.

Important Institutions

Finance Commission

Recommends sharing of taxes between Union and States and grants-in-aid.

GST Council

Decides GST-related matters and reflects cooperative fiscal federalism.

How States Finance Expenditure

States rely on:

- Own tax revenue

- GST

- Excise duty

- Stamp duty

- State goods and services taxes

- Tax devolution from Centre

- Grants-in-aid

- Market borrowings

- State Development Loans

Revenue Expenditure vs Capital Expenditure

Revenue Expenditure

Recurring expenditure that does not create assets.

Examples:

- Salaries

- Pensions

- Subsidies

- Interest payments

- Administrative expenditure

Capital Expenditure

Expenditure that creates long-term assets.

Examples:

- Roads

- Bridges

- Irrigation projects

- Schools

- Hospitals

- Power infrastructure

Why Fiscal Federalism Matters

- Supports State autonomy.

- Ensures regional development.

- Enables last-mile delivery of public services.

- Strengthens cooperative federalism.

- Allows States to respond to local needs.

- Helps balance accountability with financial capacity.

Way Forward

- Ensure predictable and transparent tax devolution.

- Increase untied grants to States.

- Give States greater borrowing flexibility with safeguards.

- Strengthen GST compensation and revenue stability.

- Improve States’ own tax mobilisation.

- Reduce excessive dependence on centrally designed schemes.

- Improve quality of expenditure by prioritising capital expenditure.

- Strengthen local governments and fiscal decentralisation.

Key Takeaway

States carry major welfare and development responsibilities, but their fiscal powers remain limited. Sustainable fiscal federalism requires greater flexibility, predictable transfers and better balance between accountability and autonomy.